Some of the links in this post are affiliate links. We may receive compensation if you click one of those links and purchase a product.

May 1 was decision day for college enrollment (or deposit day, if you’re like me and all about money). As I mentioned in a previous post, our youngest was considering two public colleges and two private colleges. The extra expense of private college (~$25,000 per year, or $100,000 for a four-year degree)* is enough to fund a multi-million-dollar retirement fund for our youngest, given the power of compounding.

*The $100,000 difference we would pay is actually lower than what others might pay, since our child got some scholarship money. If you look at the sticker price, the private colleges we looked at were $200,000 more than the New York State public colleges over the 4 years.

She picked one of the private colleges (it is the best fit for her, looking beyond just the financials) so we’re looking at an additional $25,000 per year minimum in college expenses. That additional $25,000 per year is significant right now, not just for some future retirement. Scott and I are self-employed, so we eat what we kill – i.e., we only earn based on what we sell.

The rental income from our real estate helps a lot, but we are just several years into our investments, so most of the income covers expenses and reserves. You don’t want to skimp on reserves, as we had issues with several of our properties this year. Real estate could absolutely be useful to pay for college, and I outlined how we might have done it had we started earlier building our portfolio. (Now we know for any future grandkids!).

We also have retirement accounts, which are not considered liquid assets for purposes of college financial award calculations. So colleges do not expect you to tap into these. But of course, I looked at ours, since it’s money, and since our retirement assets are by far the biggest part of our portfolio.

IRA’s cannot be tapped before age 59 and ½ without penalty, but there are a couple of options to access retirement money without the 10% early withdrawal penalty.

Should we tap our retirement accounts?

Substantially Equal Periodic Payment rule / 72(t)

You can avoid the 10% penalty if you withdraw from your IRA using SEPP (substantially equal periodic payments), also known as 72(t) payments. You would still owe income tax on the withdrawals if it’s a traditional IRA, which is what we each have. However, avoiding the 10% penalty is still significant. There is a limit to how much you can withdraw, and it’s calculated based on your life expectancy. There are different online calculators, like this one from Bankrate.

We could cover more than half of our annual college expense with a 72(t) withdrawal. However, we would be drawing from our retirement assets, paying income tax on the withdrawals, and most importantly, we would need to continue withdrawing each year until we are 59 and ½. Once you elect a 72(t) withdrawal, you’re stuck for five years or till age 59 and ½, whichever is longer.

Borrow from 401(k)

Another option is borrowing from a 401(k). There is a limit of $50,000 total per individual, so Scott and I could access $100,000 this way. However, like the IRA withdrawal, there are disadvantages to tapping the 401(k) as well.

- First of all, there is a five-year repayment period (except if proceeds are used for a primary residence, in which case you have 15 years). You have to make interest and principal payments at least quarterly, so payments would be significant.

- Secondly, you’re paying back your account in after tax dollars, and when you withdraw it finally in retirement, you’ll pay tax on those withdrawals – effectively double taxation.

- Finally, if you lose the job associated with the 401(k) , you would need to pay the loan back immediately. We won’t have this issue since our 401(k) is a solo 401(k) tied to our business, but I suppose Scott and I might try to fire each other – working with your spouse is not all roses and unicorns.

Regardless, tapping into our retirement accounts to pay for college isn’t easy, cheap or ideal. We don’t want to choose either / or. We want to keep our retirement accounts intact and find a way to pay for college.

We’ve purchased three properties in our Solo 401(k). If you are interested in purchasing real estate with your own retirement funds, you may be able to use a self directed IRA or solo 401(k). Check out Checkbook IRA.

We don’t have a college fund for our children

Before you go off the rails about how not saving a college fund is fiscally irresponsible, we did save aggressively since our first jobs, but just not in a fund earmarked for college expenses. We always prioritized retirement accounts first, then liquid accounts, where liquid would be for all major expenses. Buying a home would come first, both in priority and in life stage, and college would take what was left over.

In 2001, when our kids were 5 and newborn, we opened college savings accounts, specifically 529 accounts, to take advantage of some of the tax benefits. We also got some 529 money as a gift from a god parent. We didn’t continue with the funds, opting to throw any excess money into real estate, but over time these investments have grown to $13,000. Of course, we’ll use this to defray the upcoming college costs, but it’s less than 10% of what we need!

Another asset that isn’t a dedicated college fund per se, but acts like it, is our small pile of Series EE savings bonds, most of which we were gifted for our wedding or birthday gifts over the years. Series EE savings bonds can be cashed in for any reason but if you use savings bonds to pay for college, the interest earned may be tax-deductible. That said, we have maybe $2,000 in savings bonds so maybe enough for books, but not much else.

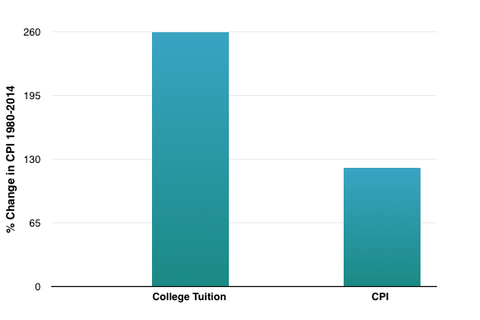

A big reason why I didn’t bother with dedicated college funds is that I assumed the crazy inflation of college expenses would fix itself by the time our kids got to college. Online education would reduce costs. Or there would be a drop-off in demand, as parents came to their senses about overpaying. Or, there would be increased supply as international schools became more attractive in our increasingly global world.

Surely, the inflation rate for college expenses couldn’t continue to exceed regular inflation and wage growth by so much more. Except, that is exactly what happened:

Our college expenses this year are ~$40,000. The merit scholarship is renewable based on a minimum GPA. The rest of the package could change year-over-year, and our costs go up if some of the financial aid is removed. I also am not sure if the total estimated expenses includes enough of a buffer for books, supplies, and other ancillary expenses. $40,000 is the minimum, but $60,000 is the outer-bound annual expense.

How will we cover up to $60,000 per year in college expenses?

The scary part about self-employment is that you earn what you sell. The fun part about self-employment also is that you earn what you sell. Now that we know how much college we have to cover, we’ll have to earn it.

Scenario 1: Build up online products

We have already launched our first online product, a job search course. Priced at just under $200, we would need to enroll 300 students per year to hit $60,000 in revenues (I’m just ignoring expenses right now to keep it simple).

Product sales and marketing would need to be in addition to all the other work we’re doing because we’d need to cover our living expenses. However, once the product is built and we have a working sales and marketing campaign going, it seems feasible to keep the product line humming along with our other consulting.

Scenario 2: Step up the consulting

Products is our focus this year to get it going, but I stay closely connected with my network to keep my consulting options open. Consulting is a time-for-money exchange so I can’t just assume I can book additional hours or accommodate additional hours. However, projects range in time commitment, rate, and upside, so depending on where we are with our products and existing projects, I may prioritize consulting.

It’s good to have options, which is why we continually try to develop our location-independent skills.

Scenario 3: Costa Rica becomes a full-time home

Another scenario we are playing with (or perhaps just me) is radically restructuring our lives and our real estate to absorb the college expenses into a much simpler life. Now that state school is out, we don’t need to worry about claiming residency in New York State. We could sell our New York place, use the proceeds to cover some of college, and decamp to Costa Rica.

Costa Rica’s much lower cost-of-living could be supported by our investments, meaning our products and consulting can cover the rest of college and/or be reinvested into our businesses. Taking day-to-day living expenses out of the equation, especially New York City level living expenses, makes a big difference.

Of course, our place in New York City is where our older daughter is living while she gets established. Our youngest also says she wants to come back to New York City upon graduation. So Scenario 3 is the most disruptive to the entire household.

We will focus on Scenario 1 first, then Scenario 2 as a back-up, and Scenario 3 only as the “nuclear option”.

======

How about you? Did you have a separate college fund in your family? How did you pay for college expenses and still stay on track for retirement?

We are Scott and Caroline, 50-somethings who spent the first 20+ years of our adult lives in New York City, working traditional careers and raising 2 kids. We left full-time work in our mid-40’s for location-independent, part-time consulting projects and real estate investing, in order to create a more flexible and travel-centric lifestyle.

We are Scott and Caroline, 50-somethings who spent the first 20+ years of our adult lives in New York City, working traditional careers and raising 2 kids. We left full-time work in our mid-40’s for location-independent, part-time consulting projects and real estate investing, in order to create a more flexible and travel-centric lifestyle.  Financial independence and early retirement is not something we originally focused on, but over time realized it was possible. Our free report,

Financial independence and early retirement is not something we originally focused on, but over time realized it was possible. Our free report,

I’m banking on the crazy rate of inflation of tuition costs to fix itself too! I have 12 more years…fingers crossed! Hoping the go to SUNY like my wife and I but who knows what will happen. We do have 529 plans but don’t save aggressively there. As to the part about double taxation of 401k loans…I don’t agree: https://thefinancebuff.com/401k-loan-double-taxation-myth.html

Hi Andrew, thanks for sharing the Finance Buff post — love the $30 example. That said, I think the post just points out how paying back your 401k loan is like paying back other loans, which you also do with after-tax money. I agree 100% with that. The difference with other loans, like non-401k mortgage loans however, is that when you do sell your house, you pay gains on the net proceeds, not the entire value of the house. For 401k distributions, you pay on the entire distribution, not just the gains. Based on the amounts I’m managing, it’s not that big a deal so I’m not going to let tax considerations lead the decision.

Substantially Equal Periodic Payment rule / 72(t)

This was exactly what I and my wife did for my daughter’s College education 2 years ago. We used the money for about 70% of her tuition that school year. No regrets, we had a situation, we did what we had to do and it was used for my childs education.

I hear you! The SEPP can be a great solution. Once you elect it, it’s forever. So what did you do with the distributions in subsequent years, if not college? Did you just reinvest after-tax?

Always a tough topic. You guys have some awesome ideas and thoughts on tackling the high cost of a college education (2x).

I graduated with well over $50,000 in student loan debt…. which I am still paying back bit by bit.

I was able to get away with under $15k, and that was manageable. I do think some debt (or needing to work) helps the student have some skin in the game. Just not so much debt that feel they have to make different career choices.

In the case of my father and I we used the US military education plan. My father volunteered for military service in 1964, and after 4 years of driving a tow truck at various USAF bases in California, came home to Brooklyn. He then got a job and used the GI Bill to get his degree. In spite of his degree, my father is a blue collar man, and my mother did secretarial work and house cleaning for extra money for the family. They saved what they could for us, but it wasn’t much. We did get a good home in a safe area with good schools in the suburbs, so my sister and I have nothing to complain about. In my case, though, I followed him and my grandfather before him into military service. In my case, I got a ROTC scholarship, and that paid most of my degree costs. I still had to pay room and board, and that meant about $20,000 in student loans.

My wife and I are in a position to put away significant funds for our son’s education. We got to a late start, so it will likely be just him, and that helps as well. In our case, we hope to have $200k, but do keep in mind that is with many years left. My son recently stopped wearing diapers. We are using a 529 account, and we put any cash presents he gets in there as well.

Yes, military funding! Great point. Neither Scott nor I come from a military family, so it isn’t an option for our kids, but it’s a possibility for others for sure. Thanks for adding that!